The Spring 2019 edition of Lifestyle Northwest by Windermere Real Estate featuring homes for sale in waterfront and island communities throughout Puget Sound is now available!

Read the online version or click the image below to download.

“Real estate transactions come and go but helping people goes on forever…”

This summarizes a cornerstone belief of Windermere’s culture. 30 years ago, we started the Windermere Foundation to propel this belief into action with the mission to support at-risk youth and members of our communities who are experiencing homelessness and difficult circumstances.

Lew Mason, the Managing Broker at our Yarrow Bay office and Eastside Windermere Foundation Coordinator, while receiving the third Bellevue LifeSpring Wings Award for outstanding community contribution.

We have been lucky enough to collaborate with over 500 organizations to facilitate this effort, including Bellevue LifeSpring. Last week we were honored to receive the third Bellevue LifeSpring Wings Award for outstanding community contribution, and we would like to take this as an opportunity to spread the word about this incredible organization.

Like the Windermere Foundation, Bellevue LifeSpring is committed to making our communities a better place to call “home.” A group of women first started the organization as Overlake Service League in 1911 to help break the cycle of poverty by providing basic needs for children in low-income families, which allowed them to focus on their education. They served Bellevue’s population of just over 150 by delivering food baskets, goats for milk, and seeds and farm equipment to plant and harvest food. During the Great Depression they also helped people find jobs.

Over a century and several population booms later, Bellevue LifeSpring’s methods and services have changed but their dedication to improving our community remains the same. Today, they partner with the Bellevue School District to provide food assistance to students, offer need-based scholarships for summer school and college, distribute vouchers for new back-to-school clothing at local merchants, and supply vouchers for year-round clothing needs at their thrift store, Thrift Culture.

We are so grateful to have Bellevue LifeSpring’s support and recognition with the Wings Award. We look forward to many more years of working together to build a better future for everyone. Find out more about Bellevue LifeSpring’s programs and how you can help here.

The Spring 2019 issue of Windermere Living showcases rising talents in interior design, spring refresh strategies, easy brunch ideas for your next get together and a helpful houseplant guide.

Windermere Living is an exclusive listings magazine published by Windermere Real Estate. Read the online version by clicking on the image below.

The spring home buying season started early this year. Open houses had increased attendance and bidding wars returned. After months of softening, home prices in most of the region jumped significantly from the prior month. With just one month of data, we’ll have to wait and see if this is the start of a longer upward trend.

Eastside

>>>Click image to view full report.

The Eastside was one area of King County that continued to see prices moderate. The median price of a single-family home on the Eastside was $900,000 in February, a drop of 5 percent from a year ago and down slightly from last month. However, supply here isn’t nearly enough to meet demand, a fact that most likely won’t change any time soon. Amazon’s latest expansion in Bellevue is expected to bring a significant wave of new employees to the city.

King County

>>>Click image to view full report.

The median single-family home in King County sold for $655,000 in February. While up slightly less than 1 percent year-over-year, it was an increase of $45,000 over January. Southeast King County, which includes Kent, Renton and Auburn, saw the greatest gains with prices rising 4.5 percent over the previous year. While inventory has grown, it is less than half of the four to six months that is considered balanced.

Seattle

>>>Click image to view full report.

More inventory and low interest rates helped bring buyers back into the market. The median price of a single-family home in Seattle hit $730,000 in February, down 6 percent from a year ago, but up $18,500 from January. With just six weeks of available supply, Seattle continues to have the tightest inventory in the county. Seattle’s record development boom shows little signs of easing, so we can expect strong demand to continue.

Snohomish County

>>>Click image to view full report.

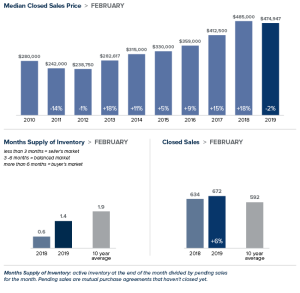

The median price of a single-family home in Snohomish County reached $474,947 in February. Although that is a 2 percent decrease from last year, it is $5,000 more than January. As buyers push outside of King County to search for more reasonably priced homes, Snohomish County continues to struggle to find enough inventory to meet growing demand.

Giving back has always been a big part of who we are at Windermere. In the early days of our company, it was pretty simple; we would see a need and help any way we could. But as we grew, we realized we could accomplish much more if we had a common purpose. That’s how the Windermere Foundation was born.

A big idea

We started with an idea that would give every Windermere agent the ability to make a difference. Housing is our business, so helping homeless families seemed like a natural fit. We later expanded that to include low-income families, with an emphasis on helping children.

Every time a home is sold

For the past 30 years, a portion of every Windermere agent’s commission has been donated to the Windermere Foundation. Having 100% participation gives us a common purpose and sends a powerful message about our commitment to the community.

Who we help

Last year alone we provided funding to more than 500 organizations throughout the Western U.S. Homeless shelters, food banks, schools, hospitals, community centers, parks; the list goes on. The main thing that they all have in common is a deep devotion to helping our neighbors in need.

How we help

Our agents have proven time and time again how committed they are to making their communities a better place to live. Their generosity funds backpacks full of food so school kids don’t go hungry on the weekends. They help keep families in their homes by covering housing costs. And their donations make sure the homeless are getting their most basic needs met, and the dignity that goes with it.

Thank you

If at any point during the past 30 years you’ve bought or sold a home using a Windermere agent, you are a part of the Windermere Foundation too, and you’ve helped make a positive difference in your community. And for that, we thank you on behalf of everyone at Windermere.

If you would like to learn more about the Windermere Foundation, please visit windermerefoundation.com.